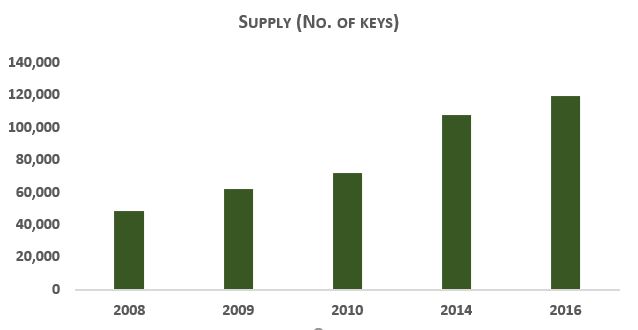

The Indian hospitality sector has observed tremendous growth in the last decade. The industry was successful in sustaining the downward pressure due to volatility caused by regular macro disturbances such as global recession, eurozone crisis, changes in local environment viz. demonetisation and implementation of GST. A study of the top 20 branded chains in India has revealed a healthy two-fold increase from 48,475 keys in 2008 to 1,19,219 keys in 2016.

With increase in spending power, the domestic tourists have been increasing continuously adding to the rising demand of hospitality sector. This has resulted in an increase in number of domestic tourist arrivals in India at ~12% (CAGR from 2014 – 2016) as recorded by Ministry of Tourism, Government of India. Further, their international counterparts have also seen a steady 7% growth for the same period.

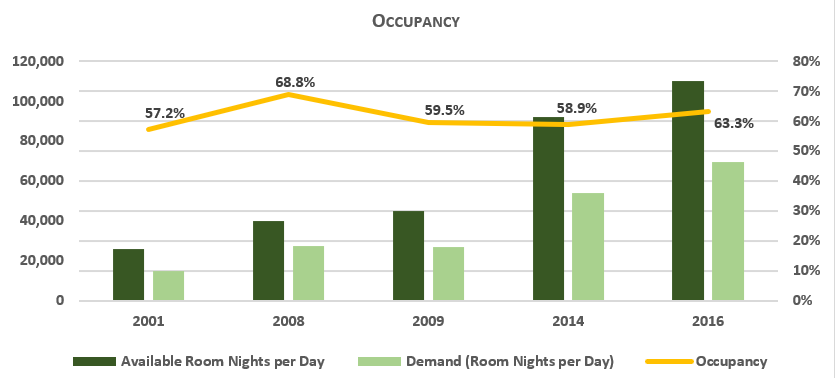

The tourist movement has outrun the supply addition and consequently, the occupancy rates of the existing hotel rooms have improved from 58.9% in 2014 to 63.3% in 2016. Furthermore, there still exists an un-catered demand across the categories in peak season.

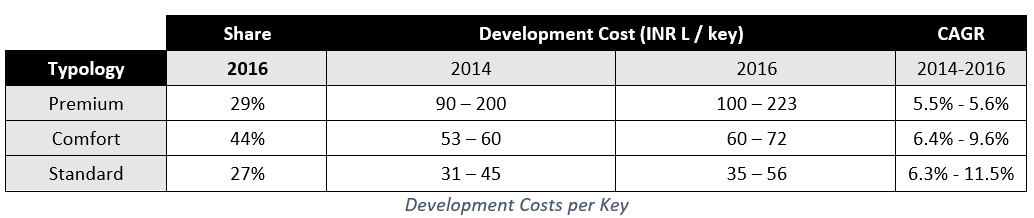

While the quantum of available rooms has increased, the revenue per available room also increased by 6% per annum. Further, a comparison of the development costs of the hotel keys indicates an average growth rate of 6.9% every year across the segments.

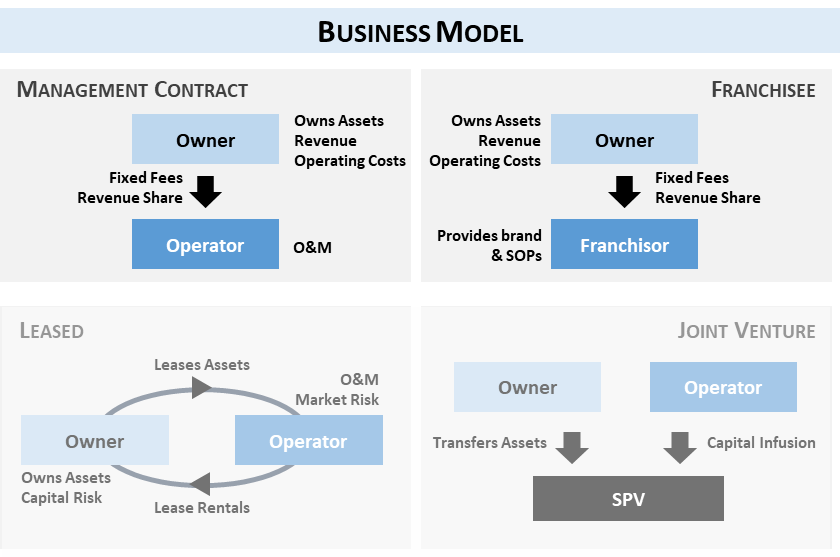

The past decade has seen emergence of Management Contract model widely across the country, wherein the private Indian investors and developers have created the assets with O&M usually outsourced to global brands. A number of international hospitality investors have forayed into the country, the major push being the security concerns and safety issues persisting in Middle East destinations such as Egypt, Israel, etc. making India a safer bet for their investments.

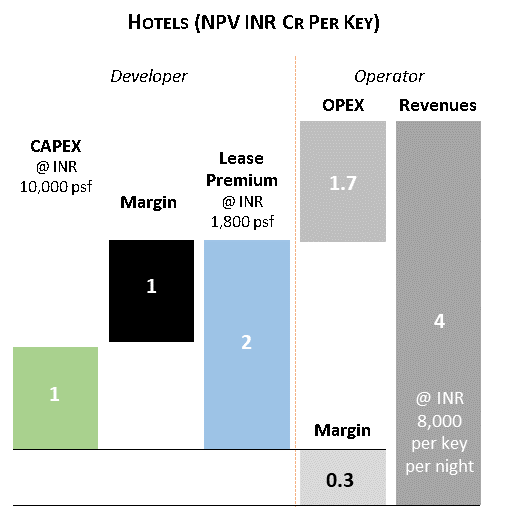

While typical management contracts have a 6-8 % revenue share as explained in the graphic below, the industry has even reported figures of 10% revenue share.